Investing is a balancing act. You’re walking on a tightrope with financial freedom on the horizon. But without a net, one misstep can mean falling — and losing it all. So how can you invest safely while maximizing returns?

A balanced investment portfolio is the net under your tightrope. It makes investing safer. We’ll show you how to create a balanced portfolio that meets your needs and keeps your money in your hands.

In this article, we’ll explore how to balance your portfolio to keep your investments safe, using:

Before we dive into that, let’s look at the fundamentals of a portfolio — and what it means to balance your portfolio.

What Is A Portfolio?

By definition, a portfolio is a collection of assets such as stocks, bonds, commodities, and more owned by an investor.

There are many types of portfolios, ranging from high risk to low risk and options in between. Choosing the right portfolio depends upon your financial goals, risk tolerance, and long-term investing strategy.

Next, let’s explore what it means to balance your portfolio.

What is “Balancing Your Portfolio”?

What does it mean to balance your portfolio?

The first rule of having a balanced portfolio is that you don’t put your money in just one place. Think of investing as a scale. It’ll never be balanced if you put everything on one side.

When you put your money in different places, you’re diversifying your investment portfolio.

For example, if all of your investment is in the stock market and it drops significantly because of things beyond your control, you might lose most of it.

When you diversify your portfolio, you are lowering your exposure to risk in one specific industry and reducing your chances of losing your entire investment.

But simply diversifying your investments isn’t enough to protect your cash. You also need to learn to balance and rebalance your portfolio.

The goal of balancing your portfolio is to make investments that align with your risk tolerance.

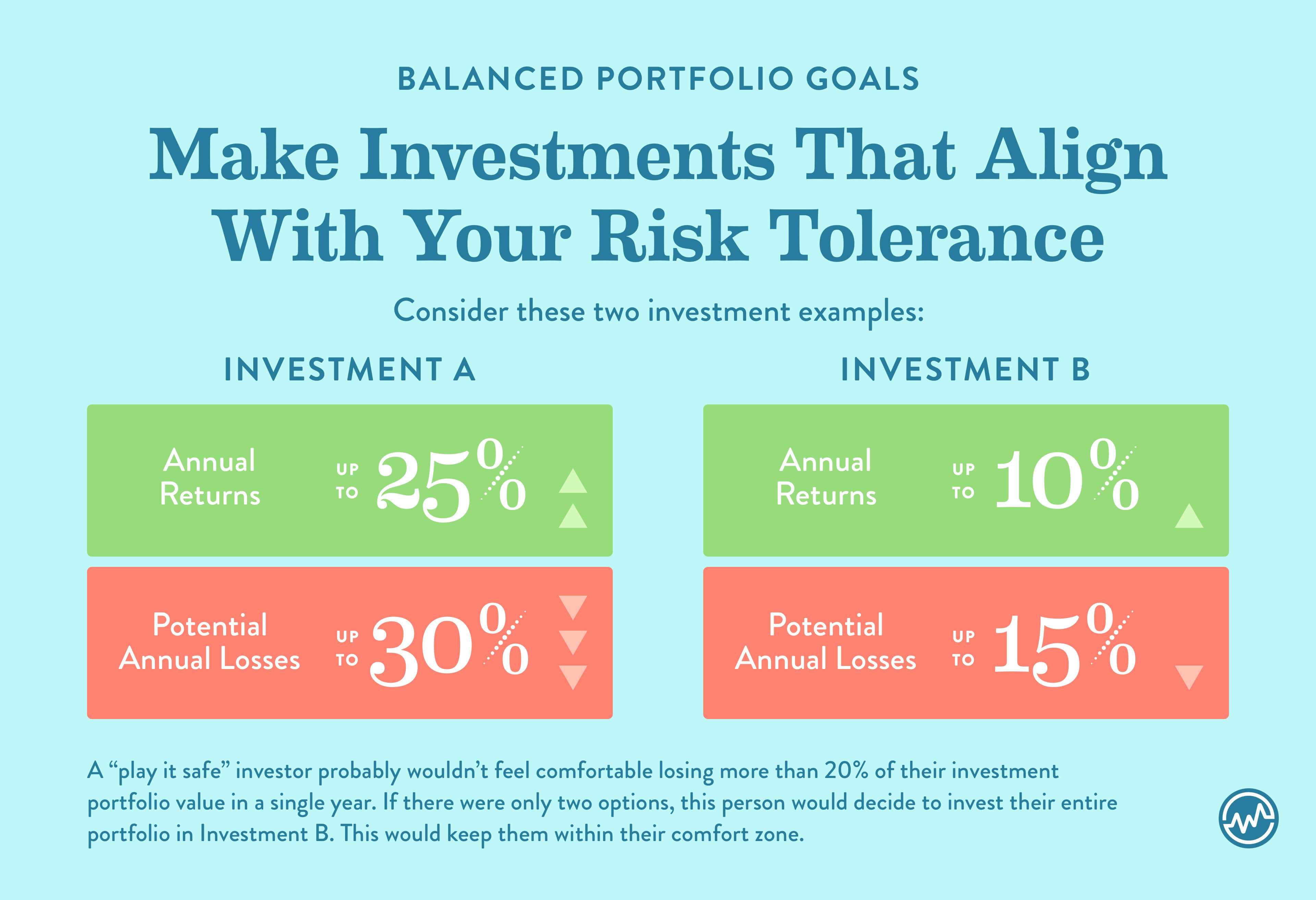

Here’s a simple example. Let’s say you have two investment options:

A “play it safe” investor probably wouldn’t feel comfortable losing more than 20% of their investment portfolio value in a single year. If there were only two options, this person would decide to invest their entire portfolio in Investment B. This would keep them within their comfort zone.

That being said, A and B aren’t their only options. And that’s a great thing.

Investment B is more conservative than this investor’s maximum comfort level. This means this person would be getting lower returns for the price of safety.

In order to increase their returns while still managing their risk, this person could balance their investments.

They can use both Investment A and Investment B together to match their comfort level. To achieve the maximum return on a safe investment, the “play it safe” investor puts two-thirds of their portfolio in Investment B and one-third of their portfolio in Investment A.

This mix increases the maximum potential returns in a year. Now, the investor can earn a maximum of 15 percent rather than the 10 percent Investment B offers.

Unfortunately, investments aren’t an open face card game. They don’t work like the textbook example above. You won’t know the maximum return or the maximum loss any investment may yield until you hit it.

That being said, you should have a good idea of the risks that come with your investments — namely the asset classes they fall into. You can also research how one asset class acts in relation to another asset class.

These relationships will help you pick suitable investments for a portfolio that matches your ideal risk tolerance.

What Are The Major Asset Classes?

You know your investment portfolio should be balanced and you have an idea of what that looks like.

Now it’s time to learn which asset classes you should use to create your perfectly balanced portfolio.

Traditionally, there are 4 major asset classes:

Each traditional asset class comes with benefits and drawbacks.

Stocks

Stocks generally offer the highest investment returns. They also have the largest potential downside with volatility.

Bonds

Bonds don’t typically perform as well as stocks do. However, they are often used to offset the risk of stocks.

Cash

While cash is the safest asset class, its returns rarely outpace inflation.

Real Estate

Real estate can help provide long-term returns. Unfortunately, compared to the other asset classes, it is more difficult to buy and sell.

Robert Kiyosak’s Asset Classes

At WealthFit, we do things a bit different: we use Robert Kiyosaki’s 4 asset classes. They include:

Kiyosaki’s asset classes expand upon the traditional asset classes.

Small Businesses

Have you seen a small business go from an idea to a money-generating machine?

You can invest in your own business or in somebody else’s business.

While small businesses can provide some amazing returns, they also go belly-up much easier than the other asset classes.

They’re much more difficult to invest in than traditional paper assets, too.

If you decide to invest in small businesses, you’re going to want to know what you’re getting into before writing a check.

It’s not enough to be interested in a project; in order to make a comfortable investment, you need a deep understanding of the following:

Paper Assets

Paper assets, another asset class, are highly liquid investments.

While they don’t provide the same outsized returns smaller businesses do, paper assets in some cases are more stable investment opportunities. Plus, investing in paper assets can be simple compared to other asset classes. They also offer tax advantages.

Paper assets include stocks, bonds, mutual funds, and cash.

They can also include:

What are the downsides of paper assets? This includes high commission fees, volatility, and a lack of control of the market.

Commodities

With commodities, you can buy and sell contracts to own assets to diversify your holdings.

Buying and selling them is more complex than traditional paper assets.

Commodities include:

Real Estate

With the last asset class, you actually have the ability to put your hands on your investment: real estate. Plus, when paying for properties, you can be creative. You can even invest with little money or bad credit.

Real estate investments can provide returns in 2 ways:

Rental properties offer monthly cash-flow where a flipped house might sell for a more immediate profit.

Also, real estate investing often requires leveraging to maximize your returns.

Asset Classes

You can mix these asset classes — small businesses, paper assets, commodities, and real estate — to create an investment portfolio that meets your needs.

How A Balanced Portfolio Helps You Make Your Money Last

So why should you try to have a balanced investment portfolio that matches your risk tolerance?

The key is optimizing the performance of your investment portfolio while keeping your investment safe.

You could technically earn more money by investing in the best asset class year in and year out — but that would take some serious foresight on your part. Not even psychics have crystal balls that good.

Instead of leaving it to luck, you should feel comfortable with the upside risk. More importantly, you must be able to stomach the downside risk.

If you invest too aggressively and sell when an asset class drops beyond your comfort level, you lose out on the potential gains that asset class can provide you.

A balanced portfolio helps you find the investments that provide the maximum gain while managing your risk for potential loss. This can help prevent you from panic selling.

Without panic selling, you’re more likely to achieve the long-term gains your investment portfolio should offer you.

What Is Rebalancing Your Portfolio?

Over time, certain asset classes will outperform. Others will underperform. This can disturb your ideal asset allocation. In fact, it will unbalance your ideal balanced portfolio.

You will not achieve your long-term gains if you don’t rebalance your portfolio. Rebalancing your portfolio Is the key to making your money last.

So what is rebalancing? Essentially, it’s the act of selling asset classes that become too big a part of your portfolio.

Then, you buy more of the asset classes that are underrepresented.

How Your Investment Portfolio Can Become Unbalanced

Let’s say your ideal balanced portfolio consists of:

One of your small business investments hits a homerun and triples in value overnight.

This could tip the scales of your balanced portfolio.

Now, small businesses might make up 75 percent of your investment portfolio. Even though your paper asset value didn’t decrease, it now only makes up 25 percent of your portfolio. The same asset class risks still exist.

If you leave your investment portfolio alone, you’re now exposed to higher risk.

That means it’s time to rebalance.

So how do you do that?

How To Rebalance Your Portfolio

To rebalance your portfolio, you’ll have to sell asset classes when they’re doing well. You’ll also need to buy asset classes that aren’t doing well.

At face value, this might not seem like a good idea. In fact, it’s actually a great idea.great idea. It forces you to sell high and buy low, which is exactly what smart investors aim to do.

In the scenario above, this means you sell some of your small business investments.

Then, you use that money to buy paper asset investments.

Once you’re back to a 60/40 allocation, you are properly rebalanced.

Achieve A Balanced Portfolio

Figuring out your ideal balanced portfolio helps you reduce your risk of making bad long-term investment decisions.

Rebalancing helps you continue to make smart decisions and grow your wealth.

The key is remembering to do both — even when things seem great.

So where do you go from here?

Take a look at your portfolio and answer the following questions:

As always, you should consult with a financial advisor when making any investment decisions.

Continued Learning: Investing

Now that you know how to balance your investment portfolio with small business, paper assets, commodities and real estate and how to rebalance it if needed, here are a few other free resources to continue your financial education: